Courtesy of The Economist, a look at how China’s wild-east stockmarkets are more suited to cowboys than to Oracles from Omaha:

AS THE second-richest person in the world, and with a half-century record of investing success, Warren Buffett is a household name worldwide. But in China, he is something more: a celebrity. In March a special edition of Cherry Coke, featuring a cartoon image of the 86-year-old investor, hit Chinese shop shelves (Mr Buffett not only loves the sugary beverage; he is Coke’s largest shareholder). On May 6th thousands of Chinese investors will descend on Omaha for the annual meeting of Berkshire Hathaway, his holding company, and many more will tune into a live-stream of the event. Mandarin is the only foreign language into which the proceedings will be simultaneously translated. Those who miss the broadcast can pick up one of the hundreds of Chinese books about his approach to minting money.

Mr Buffett’s stature in China stems partly from good timing. China’s modern stockmarket was launched in 1990. Just as neophyte investors grappled with earnings reports and trend lines, the Oracle of Omaha’s reputation as the world’s best stock-picker was blossoming. Compared with the regular booms and busts of the Chinese stockmarket, the steady returns of Berkshire Hathaway are beguiling. For Chinese investors who do make it big, there are few greater accolades than to be dubbed the “Warren Buffett of China”. This title has been conferred on or claimed by no fewer than ten tycoons.

But they might want to think twice. In the Chinese context, declarations of Buffett-like investment abilities have, over the past couple of years, proved less a badge of honour than a warning sign. In rapid succession his putative disciples have run into trouble. One was jailed for manipulating the stockmarket. A second has been held incommunicado in custody for months. A third was hauled in as part of a government investigation.

This chasm between the veneration for Mr Buffett and the travails of those who supposedly model themselves on him points to the messy reality of Chinese finance. Investors are becoming more sophisticated, with professional fund managers, once marginalised, playing a bigger role in the country’s markets. Mr Buffett is held up as the gold standard of value investing, respected for his long-term view in selecting stocks. But when they get down to business, many Chinese investors still opt for hard-driving, debt-laden, risky approaches; they are products of a stockmarket that is not yet three decades old and an economy that during that time has seen few serious downturns.

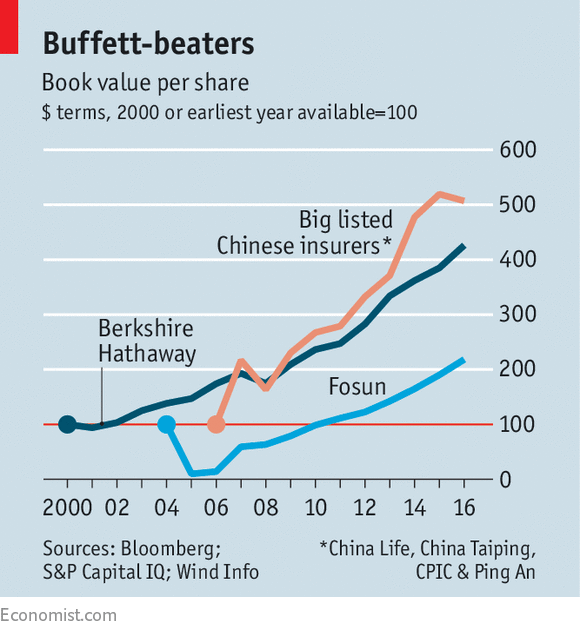

Consider the two investors most often likened to him. One is Guo Guangchang, chairman of Fosun, a conglomerate with interests from mining to tourism. There is a superficial similarity between Fosun and Berkshire Hathaway in that both partly pay for their investments by selling insurance. But the contrasts are just as striking. Over the past decade Berkshire Hathaway has been able to finance more than four-fifths of its investments with cashflow from its operations; Fosun’s cashflow has covered less than a quarter of its investments. The result has been a much higher reliance on debt for the Chinese firm.

Another Chinese investor described as applying the “Warren Buffett model” is Wu Xiaohui of Anbang. Anbang’s insurance business has surged over the past five years, with its assets reaching 1.9trn yuan ($286bn) in 2016, more than triple their 2012 level. Anbang, like Berkshire Hathaway, has financed most of its investments with revenues from selling insurance. But unlike Mr Buffett’s stable business, Mr Wu has relied on the sales of short-term, high-yielding insurance policies, tantamount to a hidden form of debt.

These Chinese Buffetts now face a stiff test. The government appears at last to be serious about cleaning up financial markets after a decade of runaway debt growth. Regulators have repeatedly promised to rein in credit issuance, only to back down when the economy has slowed. In recent months, though, they seem to be mounting a more sustained onslaught. Xi Jinping, China’s powerful president, has declared that the focus of financial policy should be on limiting risks. The securities regulator has vowed to catch the “giant crocodiles” feasting on the savings of ordinary investors. And the banking regulator has unleashed what the local press has called a “tightening storm”, choking off cashflows to shadow banks.

The risk to Chinese investors is twofold. The first is political. The state is closing in on those it suspects of illegality. Xu Xiang and Xiao Jianhua, managers of secretive investment companies, won accolades as Chinese Buffetts for no reason other than their good returns. Both are now in detention: Mr Xu was jailed for manipulating the stockmarket; Mr Xiao is being held as part of a corruption investigation.

The second risk is financial. In clamping down on debt, regulators’ targets are the debt-laden investments favoured by China’s insurance upstarts. Both Fosun and Anbang have had to call off foreign deals in the past year. On May 3rd Anbang said it would sue Caixin, a business magazine, over allegations of financial irregularities.

Lost in all the hype about these supposed Buffetts of China is that there are in fact companies which have been more Buffett-like: big, boring, mainly state-owned insurers. Hewing to official rules, they have been more cautious about using debt. Benefiting from China’s growth, their performance (measured by book values per share, Mr Buffett’s preferred gauge) has topped Berkshire Hathaway’s over the past decade, albeit with more ups and downs (see chart). They also share one other trait with Mr Buffett, who is famed for his humility. They have not boasted about their success.

This entry was posted on Saturday, May 6th, 2017 at 8:18 pm and is filed under Uncategorized. You can follow any responses to this entry through the RSS 2.0 feed.

Both comments and pings are currently closed.

Global Buffetts is dedicated to compiling a compendium of elite international money managers & investors. While the U.S. is indeed home to a number of world-class financiers, the rapid economic development and dynamic rise of financial acumen around the world has changed the playing field in the past decades. There are now a number of global "Buffetts" plying their trade & demonstrating their expertise in their own markets. Often, however, there is little written about such individuals as most popular media is focused on the big names in U.S. investing. This personal interest blog is one individual's attempt to uncover other elite money managers from around the world.

Educated at Yale University (Bachelor of Arts - History) and Harvard (Master in Public Policy - International Development), Monty Simus has lived, worked, and traveled in more than forty countries spanning Africa, China, western Europe, the Middle East, South America, and Southeast & Central Asia, and his personal interests comprise economic development, policy, investment, technology, natural resources, and the environment, with a particular focus on globalization’s impact upon these subject areas. Monty writes about frontier investment markets at www.wildcatsandblacksheep.com and geopolitical pressures in the global agricultural sector at www.seedsofarevolution.com.